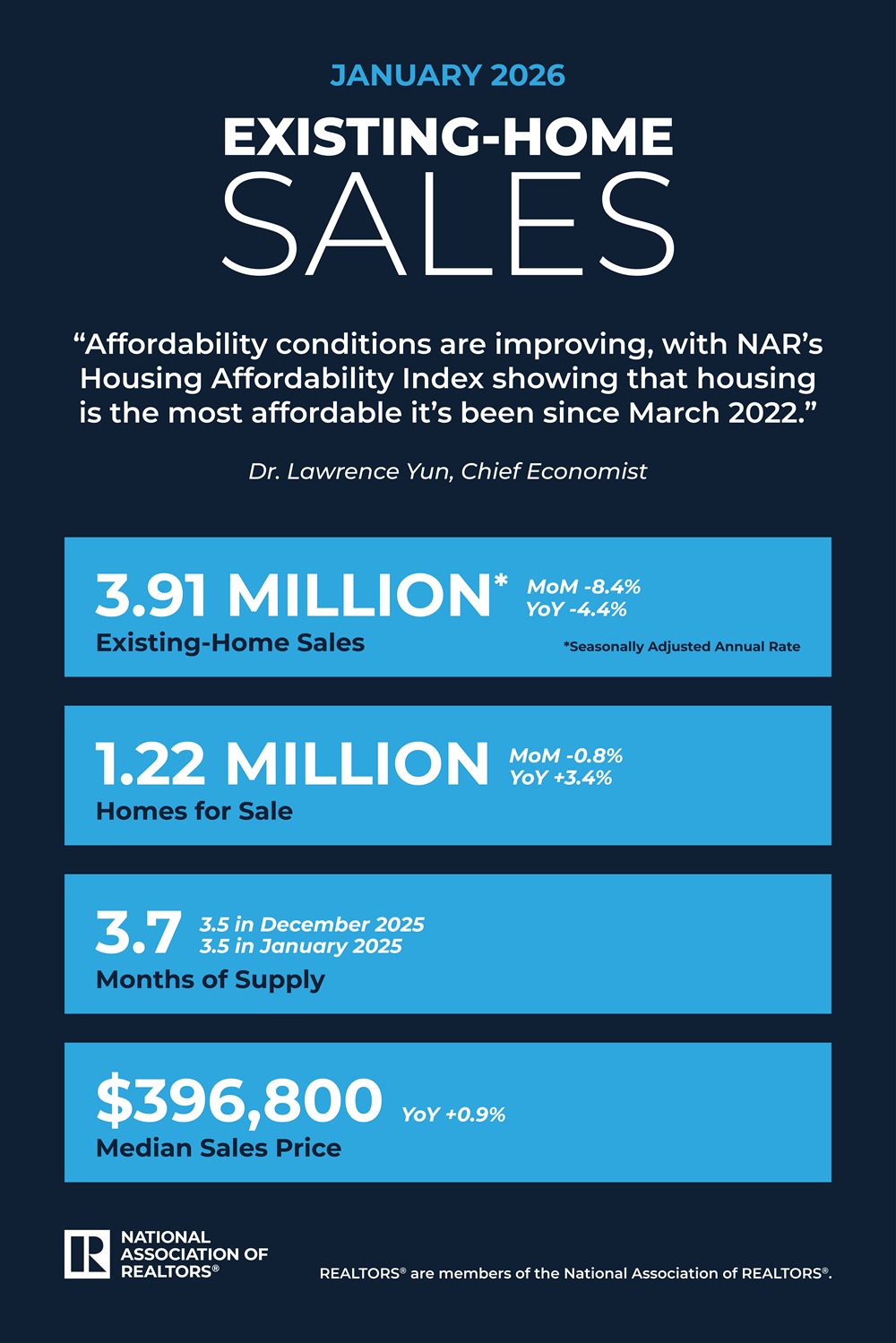

Existing-home sales decreased by 8.4% in January, according to the National Association of REALTORS® Existing-Home Sales Report.

Month-over-month and year-over-year sales fell in all regions.

“The decrease in sales is disappointing. The below-normal temperatures and above-normal precipitation this January make it harder than usual to assess the underlying driver of the decrease and determine if this month’s numbers are an aberration,” said NAR Chief Economist Dr. Lawrence Yun. “Affordability conditions are improving, with NAR’s Housing Affordability Index showing that housing is the most affordable it’s been since March 2022. This is due to wage gains outpacing home price growth and mortgage rates being lower than a year ago. However, supply has not kept pace and remains quite low.”

“Due to low supply, the median home price reached a new high for the month of January,” Yun added. “Homeowners are in a financially comfortable position as a result. Since January 2020, a typical homeowner would have accumulated $130,500 in housing wealth.”

Affordability improved for the seventh consecutive month, according to NAR’s Housing Affordability Index—increasing to 116.5 in January from 111.6 in December and 102 a year ago.

Total Existing-Home Sales

- 8.4% decrease in existing-home sales month over month to a seasonally adjusted annual rate of 3.91 million.

- 4.4% decrease in sales year over year.

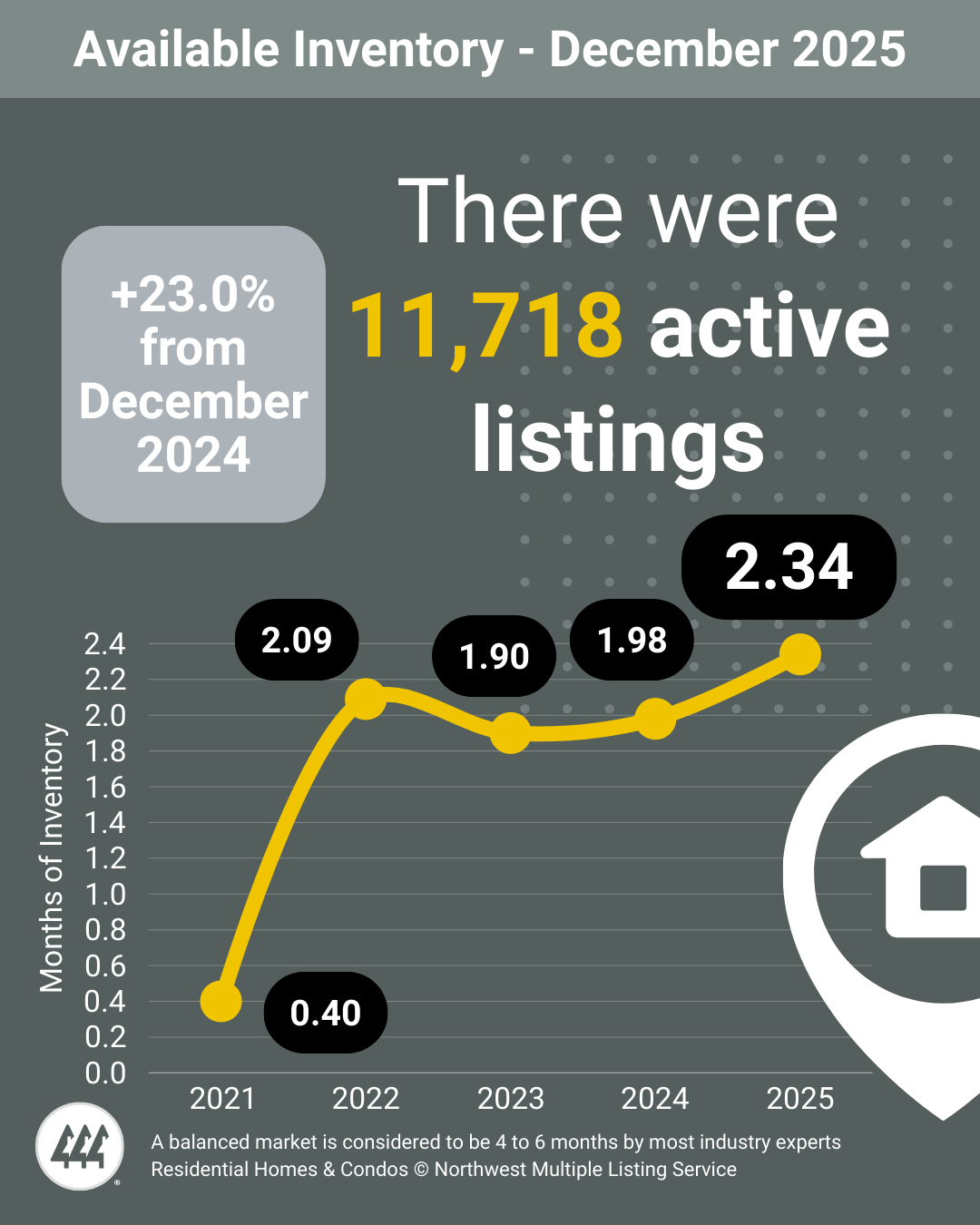

Inventory

- 1.22 million units: Total housing inventory, down 0.8% from December and up 3.4% from January 2025 (1.18 million).

- 3.7-month supply of unsold inventory, up from 3.5 months in December and one year ago.

Median Sales Price

- $396,800: Median existing-home price for all housing types, up 0.9% from one year ago ($393,400) – the 31st consecutive month of year-over-year price increases.

Read more details, including regional data, here…

Source: National Association of REALTORS® 2/12/26